Music: This video discusses the Tax Cuts and Jobs Act repeal of Section 958(b)(4) regarding downward attribution to a U.S. corporation. - The change was intended to prevent inverted companies from controlling their controlled foreign corporations (CFCs). - For example, let's say that a U.S. parent company, USP, owns 100% of CFC. - USP inverts so that it now has a foreign parent, FP. - We will assume that FP is not a surrogate foreign corporation under Section 7874. - After the inversion, USP would like to avoid subpart F income earned by CFC. - In an attempt to avoid the subpart F income, FP invests cash or property into CFC in exchange for newly issued shares in CFC. - As a result, FP owns 51% of the shares, while USP now owns 49% of CFC. - Under the old attribution rules, CFC would no longer be considered a controlled foreign corporation since the shares owned by FP were not attributed to USP. - However, with the new change in law, the 51% of CFC shares owned by FP will be attributed to USP. - This is because USP directly owns 49% of the shares and constructively owns the remaining 51%. - Therefore, CFC will continue to be a controlled foreign corporation. - As a controlled foreign corporation, USP will need to continue filing Form 5471 on an annual basis as a category 5 filer and report its proportionate share of any subpart F income. - Music.

Award-winning PDF software

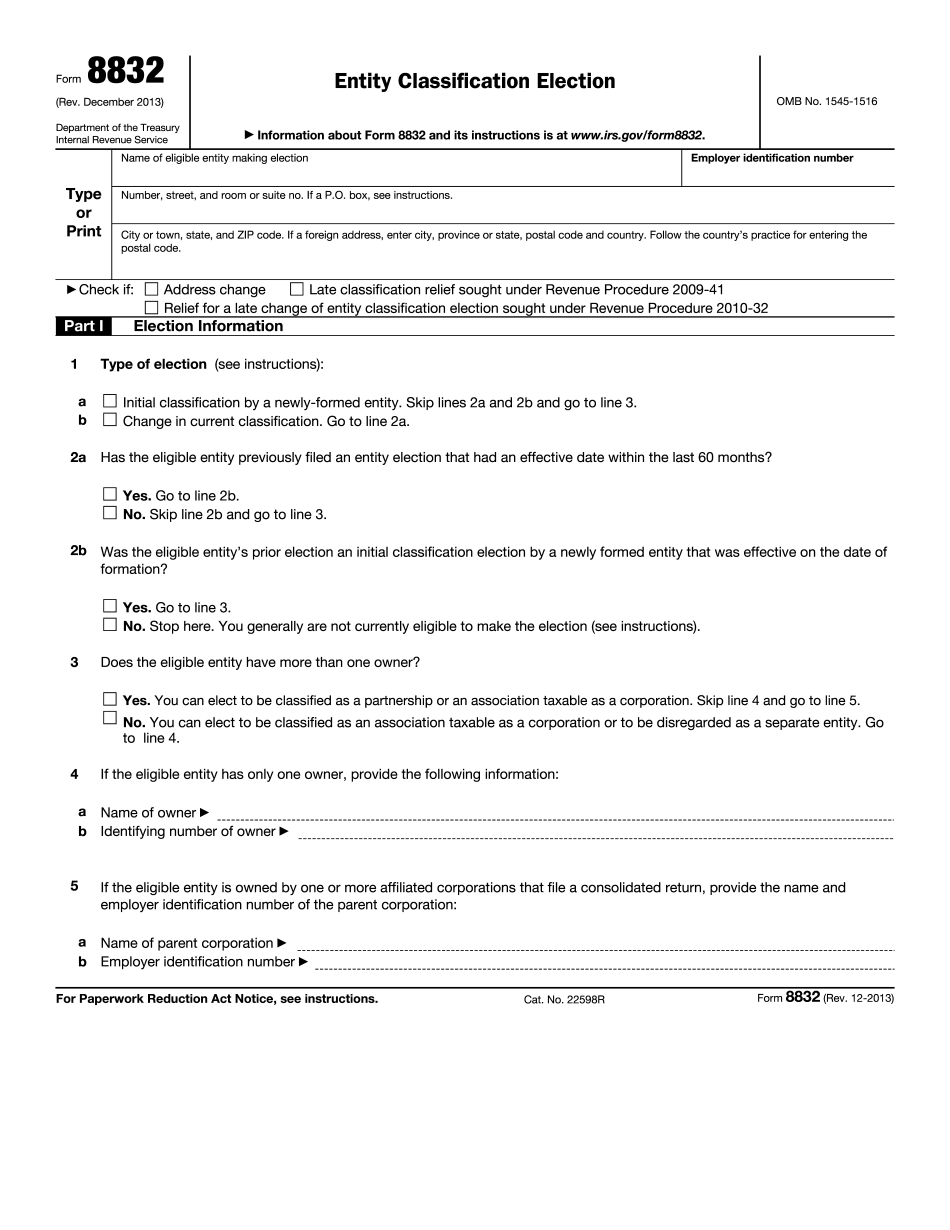

Revoke s corp election retroactively Form: What You Should Know

Tax-Exempt Organizations | IRS Support This is not an IRS e-file support page. Please call our Help Desk 611. Tax Exempt Organization Election — IRS The “Organization Exemption Application” form requires 2 pieces of information and must be signed by at least one officer of the organization. One document must be provided in advance to the IRS. One can be sent electronically. Both documents must be received by the IRS by April 25, 2025. Tax Exempt Organizations IRS e-file service for Tax Exempt Organizations. In order to successfully e-file the required documentation in order to obtain tax-exempt status, an organization needs to submit 1) the form 8283, Application for Authorization (Form 8283A), as part of the application for status as a tax-exempt organization, and 2) a copy of each of the documents described in instructions below. The form 8283 is required if you seek to file a new status petition for a tax-exempt organization. A tax-exempt organization (OTC) becomes a tax-exempt organization (TO) when it files Form 1023. The IRS e-file service allows the organization to file electronically, receive certification(s) from the IRS, and receive the tax-exempt status notification. The “Certification” page of the e-file site also provides a form to submit electronically that will allow the organization to certify that the filing is complete. E-filing for Tax-Exempt Status—Vista Business Solutions This form may be requested by the non-profit organization, not by a Tax Exempt Organization. It will give the IRS permission to receive tax-exempt status notification and a copy of the Form 8283. Tax Exempt Organizations—Vista If an organization has already filed Form 8283 and received certification, it may file a new version of Form 8283 using this same form. If you have previously filed Form 8283 in the past but do not know the name of the organization, the name of the entity is shown. TO/OTC — If the corporation you are applying to become has already filed a Form 8283A and received certification, it may file a new Form 8283 using this new form. If you have previously filed Form 8283 in the past but do not know the entity, it is shown on the “Organization Exemption Application” page.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 8832, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 8832 Online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 8832 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 8832 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Revoke s corp election retroactively